Cereals in Europe: global demand, environmental constraints and technologies to sustain productivity

By Juan Vilar, economics expert, international agronomic analyst, strategic consultant, professor at the University of Jaén and farmer.

The European cereals sector continues to play a strategic role within the global agri‑food system. Despite representing just 6.6% of the world’s cereal‑growing area, the European Union retains significant weight in international trade, particularly in soft wheat, barley and durum wheat, three crops that underpin internal supply flows and market equilibrium.

In a context marked by growing global demand, rising production costs, increasing climate volatility and a progressively stricter regulatory framework, European cereal production is undergoing a phase of structural adjustment, where efficiency and sustainability are becoming decisive criteria for future competitiveness.

Configuration of the European cereals market: a decade of structural adjustments

Of the 5.1 billion hectares of agricultural land worldwide, cereals account for around 15% (≈750 million ha). In Europe, the 50 million hectares devoted to these crops have shown a downward trend since 2014.

Production trends and determining factors

The all‑time record of more than 300 million tonnes in 2014 has given way to an estimated ≈258 million tonnes in 2024, the lowest level in ten years.

The reduction in cultivated area (–9.5%, equivalent to 5.2 million ha) is the first factor explaining this contraction.

The second factor is the increasing exposure to climate risk, reflected in:

- Years with sharp drops in yield due to severe drought or heatwaves

- Partial rebounds in seasons with more favourable conditions

- Growing regional variability: the north–south gradient is intensifying

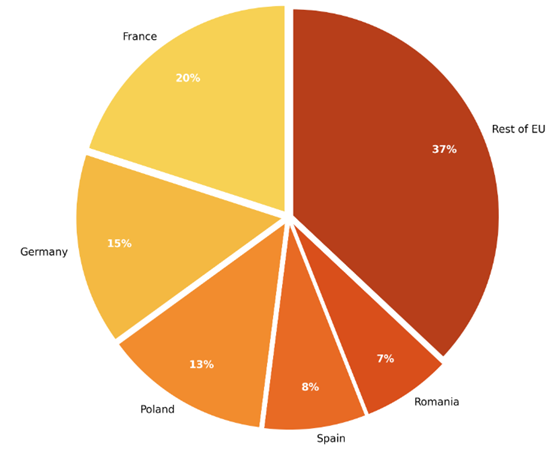

Productive leadership and geographical concentration

Five countries account for more than 50% of total volume:

- France: ≈20% (≈54 Mt)

- Germany: ≈15%

- Poland: ≈13%

- Spain: ≈8%

- Romania: ≈7%

This distribution reveals two parallel realities:

- Europe retains scale, particularly in wheat

- Surplus capacity has tightened, increasing market sensitivity to climatic or geopolitical shocks

Environmental restrictions: regulatory pressure on nitrogen and resource‑use efficiency

European cereal productivity is increasingly shaped by the regulatory environment. The Nitrates Directive (91/676/EEC) sets strict limits —170 kg N/ha/year in vulnerable zones— which directly affect fertilisation planning.

This is complemented by the Farm to Fork Strategy, which sets a minimum 20% reduction in fertiliser use by 2030, supported by:

- Precision farming

- Greater traceability

- Diversified rotations

- Improved nitrogen use efficiency (NUE)

These policies not only raise compliance requirements but also push the production model towards low‑input, high‑efficiency systems, where relying solely on increasing fertiliser application is no longer a sustainable path to maintaining yields.

Innovation and efficiency: the growing role of biostimulants in arable crops

Agricultural biostimulants are becoming one of the key technologies for sustaining cereal productivity under nitrogen limitations and abiotic stress.

Key agronomic advantages in cereals

-

Increased nitrogen use efficiency (NUE)

-

Improved root development and plant metabolism

-

Greater tolerance to drought, heat stress and water variability

-

More stable yields under constrained input scenarios

The European market is growing at 10–12% annually, driven by the regulatory consolidation of Regulation (EU) 2019/1009, which harmonises quality and safety requirements for biostimulants.

How to sustain productivity without compromising sustainability?

In this context, innovation becomes decisive. Biostimulants stand out as crop‑specific tools for arable systems, capable of enhancing nutrient uptake and optimising cereal development.

TerraSorb® granum is notable for its ability to:

- Optimise nitrogen assimilation, even when applied units are lower

- Increase the crop’s physiological resilience under stress scenarios

- Help maintain or increase yield without raising environmental impact

Its formulation makes it particularly effective in winter cereals —wheat, barley and oats— where thermal stress windows and nitrogen availability in early stages largely determine final yield potential.

Conclusion: towards a more resilient, efficient and regulated European cereals model

Cereal production in Europe is undergoing a structural transformation shaped by:

- Reduced cultivated area

- High climate vulnerability

- Nitrogen input reductions mandated by regulation

- The need for greater efficiency and traceability

- Growing global demand for stable and sustainable grain

In this environment, adopting technologies such as biostimulants is not an add‑on but a strategic lever to:

- Maintain productivity

- Reduce per‑hectare costs

- Comply with regulation

- Improve year‑to‑year stability

- Differentiate in markets demanding verifiable sustainability

The new European cereals agriculture is moving towards greener, more precise and technologically integrated systems, where competitiveness will depend not only on yield but also on producers’ ability to manage resources with maximum efficiency.